Three Major Differences Between a Broker and Fiduciary Plan Sponsor

For plan sponsors, managing a 401(k) plan can be complex and time-consuming. Some plan sponsors hire outside advisors to help the plan stay compliant with the various IRS and ERISA regulations. When hiring outside advisors, many plan sponsors are unaware of the added benefits of hiring an investment fiduciary as opposed to a broker to manage their plan investments. Each has a unique set of regulatory standards governing their behavior which can affect the range and quality of services offered to the plan. Below are a few key differences between brokers and fiduciaries:

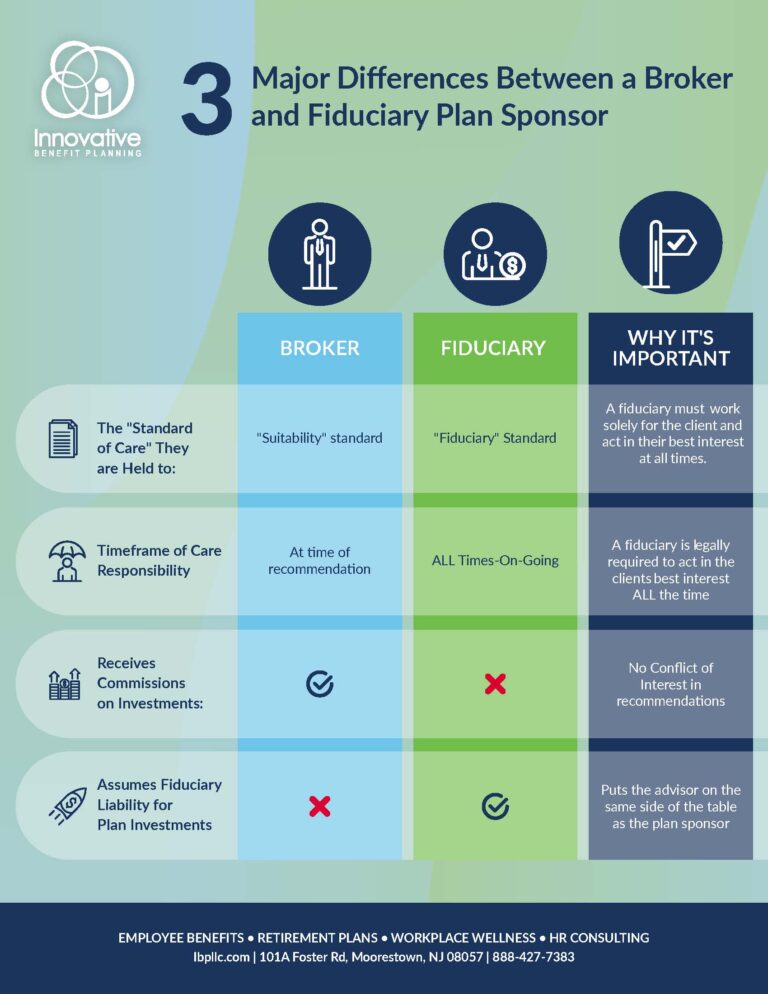

- Standard of Care:

- Brokers: Are held to a suitability standard. Under this standard, brokers can only recommend investments that they reasonably believe are appropriate at the time of the recommendation.

- Fiduciaries: Are held to stricter rules, known as the fiduciary standard of care. This standard legally requires the advisor to act in the best interest of the investor at all times, not just at the time of the initial recommendation. Therefore, it is an ongoing responsibility.

-

Commissions or Fee Based?:

- Brokers: Can receive commissions on the investment products they sell to investors. A conflict of interest could arise if a broker recommends an investment that pays a commission in lieu of a better investment that does not pay a commission. As plans sponsors, it is important to avoid conflicts of interests.

- Fiduciaries: Can only be paid through fee-based compensation. They cannot receive commissions, eliminating conflicts of interest on investment recommendations and other plan level decisions.

-

Service Quality:

- Brokers: Since brokers and fiduciaries are held to different legal standards, the level of service provided can vary. Conflicts of interest can affect the types of products and investments recommended on the plan. Since the suitability standard is less strict than the fiduciary standard, a broker does not have the same requirement as a fiduciary to monitor investment performance and fees at all times.

- Fiduciaries: Are legally obligated to provide the highest standard of care when advising on a retirement plan. When working with the plan sponsor, a fiduciary assumes a liability for the performance of plan investments, putting the advisor on the “same side of the table” as the plan sponsor.

Innovative Investment Fiduciaries, LLCis a CEFEX certified advisory firm works solely with qualified and non-qualified retirement plans for not for profit and for profit employers. For more information about Innovative’s services, feel free to contact us here or call us at (888) 427-7383.